Oleksandra Yagello | Moment | Getty Images

In many respects, conditions are good for U.S. small businesses.

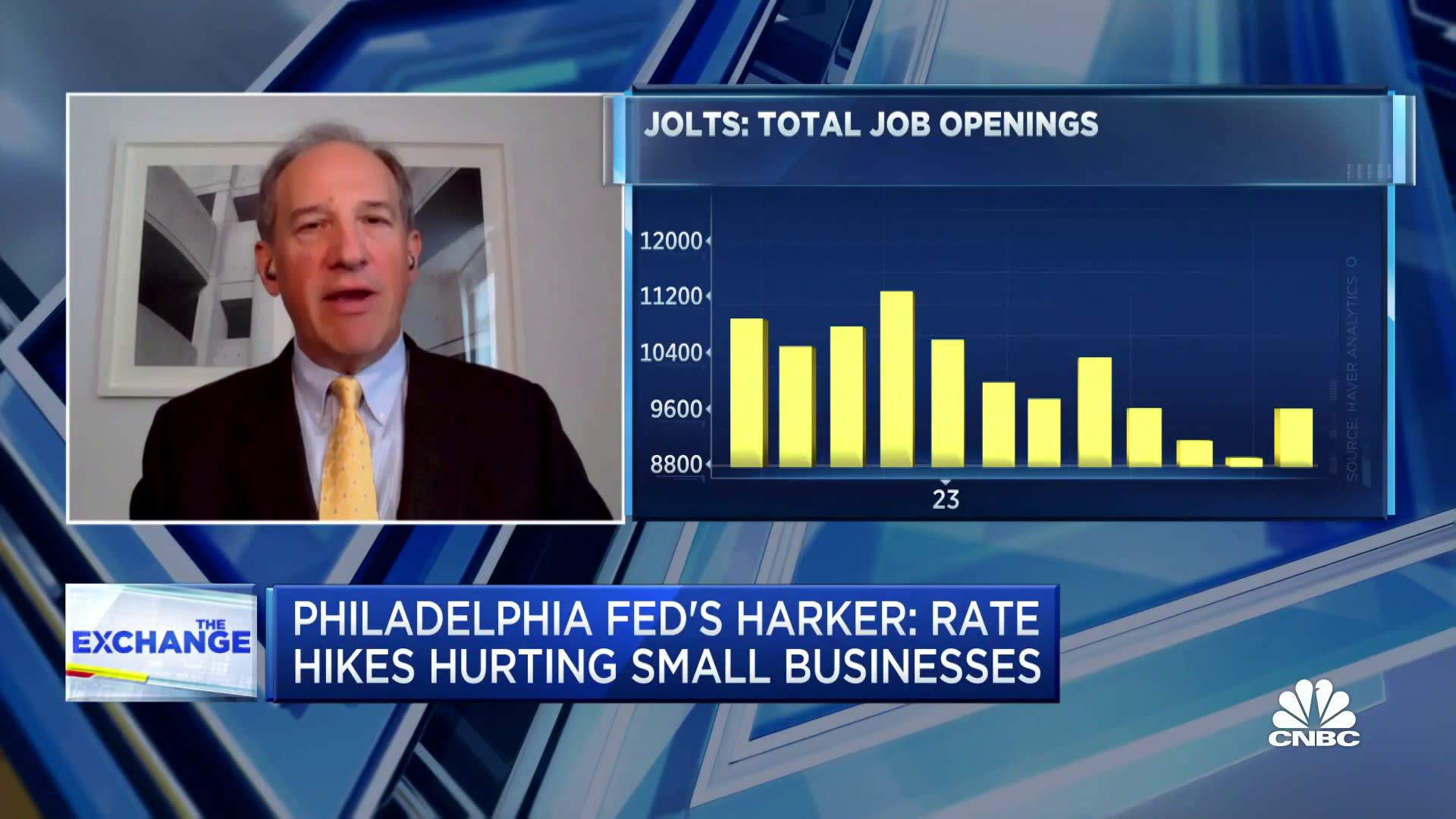

Inflation, from the cost of goods to wage growth in the labor market, are coming down. And the economy is growing like gangbusters, with the most recent GDP reading outperforming expectations, a fact that the Federal Reserve noted in its FOMC meeting statement on Wednesday when it decided to hold its key federal funds rate in a target range between 5.25%-5.5%, where it has been since July. Small businesses in certain sectors are clearly benefitting from the economy and a consumer that continues to spend, such as leisure and hospitality, with the Bureau of Labor Statistics JOLTS report released on Wednesday showing slightly higher than expected job openings in September concentrated among smaller firms.

But there’s one issue where business owners will continue to struggle, even if rates don’t go up from here — and especially if rates remain high for an extended period of time. That’s the use of high-interest credit to fund business expenses.

The “higher for longer” rate environment is the expectation in the market and on Wall Street — with the Fed in no hurry to bring rates back down, still fearing inflation even if its peak is well past. During his press conference after the FOMC meeting, Fed Chair Jerome Powell said that a decision to not raise rates now in no way means it would be any more difficult for the Fed to hike again if conditions warrant it, and that the Fed continues to believe the economy needs to see slower growth. He also said the FOMC is “not thinking about rate cuts right now at all.”

The current interest rate environment has pushed the interest level on the majority of small business loans to the double digits for the first time since 2007, and bank willingness to lend to smaller firms is being restricted among tighter financial conditions. It’s no surprise then that swiping credit cards to help fund a business has become a more common option amid a challenging economic environment, but it can be a risky move.

The average monthly credit card expenditure of U.S. small businesses is up by an average of 20% compared to pre-pandemic levels, according to a recent report by Intuit QuickBooks. While that data was only available through May, the Fed had raised rates aggressively by then and made subsequent hikes as recently as July. Ufuk Akcigit, a professor of economics at the University of Chicago who leads the development of the small business report with Intuit QuickBooks, said that that number is now likely higher.

Business bankruptcies are up, access to capital is at a low

Data from J.D. Power shows that the percentage of small businesses that plan to increase spending on their credit card in the next 12 months has moved higher, from 25% in 2022 to 28% in 2023. Credit card balances for Americans overall recently topped $1 trillion for the first time ever, and small businesses are among the most vulnerable to issues caused by high interest rates, increased threats to cash flow from higher interest payments and lack of other capital raising options. Around 1,660 small businesses have filed for bankruptcy in 2023 so far, which is higher than in all of 2022, according to the American Bankruptcy Institute.

Access to capital for small businesses is at an economic cycle low. A recent Goldman Sachs survey found that 78% of small business owners are concerned about their ability to access capital, while 53% say they can’t afford to take out a loan in the current interest rate environment. Maybe most alarming, 21% said they would close their business if the credit market doesn’t becomes less restrictive.

Getting a business credit card is much easier than getting a loan from a bank, Akcigit said.

“Lenders are typically getting more careful about who to lend to and they perceive small businesses as a more risky group,” Akcigit said, and he added that if small businesses don’t have a better option, they’re going to rely on credit cards.

Thanks to the high annual percentage rates (APRs) on credit cards, here is what business owners need to know about relying on a card to keep a business going.

You must be able to meet monthly payment obligations

The small business credit card is an important tool for credit purposes and managing cash flow — as long as the business can continue to meet its monthly payment obligations while maintaining inventory and service delivery, according to John Cabell, managing director of payments intelligence at J.D. Power, who leads research on small business credit cards at the firm.

“Where it becomes more problematic is if there is accumulating debt that cannot be paid down or resolved within a reasonable time frame,” Cabell said.

While using credit cards is typically an expensive way to take on debt thanks to the high rates set by issuers, the Fed’s rate hikes have taken the average credit card interest rate in the U.S. to 24.45%, according to LendingTree. Even in a world of much higher business loan rates, making charges to a card is likely going to be a much more expensive way of getting credit if you can’t pay it off every month.

If business is slowing down and expenses aren’t cut, covering those expenses with a credit card can be risky, said Derrick Longo, a wealth planning professional at Exencial Wealth Advisors.

“If you keep going down that rabbit hole and if your top line income doesn’t increase, and you keep saying ‘the industry will pick back up, we’ll be fine tomorrow’ and you’re not fine tomorrow, then you have a problem that sometimes you can’t dig yourself out of,” Longo said. “It could severely hurt a business.”

The risk also increases if you’re personally liable for the debts of your small business, for example, if your business is set up as a sole proprietorship or general partner.

How to properly plan with a business credit card

But proper use of a business credit card can be to the benefit to a small business owner.

“Credit used correctly can be a phenomenal tool for businesses,” Longo said. He recommends only using it to fill the gap of cash flow between when money is coming into the business and money is going out.

For example, if a billing issue with a partner company means that there is a three-month lag in expected funds, using a credit card may make sense. Just be sure you’re aware of how much money you have on hand, Longo said, since economic environments are cyclical and revenue can drop.

Business owners get card perks, too

Credit cards can also provide perks that may benefit your business overall.

If you have the ability to pay off your balance each month, there can be upsides to using a credit card in the form of cash back savings, points and rewards, said Ryan Halliday, managing partner at Crewe Advisors. The Capital One Spark Cash Plus, for example, currently offers 2% cash back on every eligible purchase, while points on Chase’s Ink Business Preferred Credit Card are worth 25% more when you redeem for travel through Chase Ultimate Rewards.

“The key is you have to have a business plan in place and have the real determination to stick to that plan,” Halliday said. If you won’t be able to stay on top of your payments, those perks aren’t worth the risk, he said.